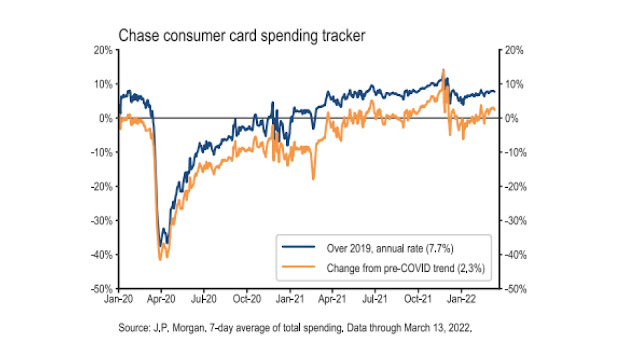

Update #10: 美國房市,企業對目前景氣看法

美國房市 房市對利率最敏感,先看看美國房貸利率走勢,今年快速攀升。 但拉長來看,目前4%根本是小菜 房貸利率還是歷史低水位,但在預期未來升息跟漲價的心理下,房價仍然往上衝,看到房地產資訊網站RedFn說的 The median home sale price rose 3.5% between January and February, the fastest month-over-month gain ever seen during the winter months. Prices were up 16% year over year to an all-time high of $389,500 in February as the number of homes for sale fell to another new low. The lack of inventory is holding back home sales, which fell 4% from January. An acute shortage of homes for sale continues to stymie buyers in the current market,” said Redfin chief economist Daryl Fairweather. “Rather than dropping out of the housing market, homebuyers only seem to be getting even more voracious, driving prices up at a startling clip. Typically, rising mortgage rates weaken demand for homes—we don’t see demand weakening yet, but we will be watching to see if buyers back off or remain steadfast amidst rising borrowing costs. 搶購潮仍然有 雖然RedFin沒看到房市需求轉弱,但實際數據是有掉的,美國2月的成屋銷售MOM下滑7%,因為每月的付款年增28...